Seasonality is returning to lift the VLGC spot market, but after three years of rates in the doldrums, the forecast remains mixed as to when the clouds will lift from the sector.

The third quarter is traditionally stronger for the vessels and rates have moved above break-even, with a helping hand from geopolitics.

Analysts at DNB Markets placed VLGC spot rates at $24,406 per day on Monday this week, which is above its cash break-even expectations for new VLGCs.

The summer uplift follows a slack start to the year blamed on newbuilding deliveries and reduced tonne-mile demand due to Middle East exports displacing some of the longer-haul shipments from the US to Asia.

According to Clarksons, concerns over potential disruptions to supply, driven by impending decisions on US sanctions and trade tariffs, have helped the market. Importers have been looking to build inventory levels, while US export volumes have recovered.

“Traditionally, the market tends to show some seasonal strength over the summer months and, although we have seen this reversed over the last few years, we may be witnessing the start of a return to this pattern,” Clarksons said in its first-half report this week.

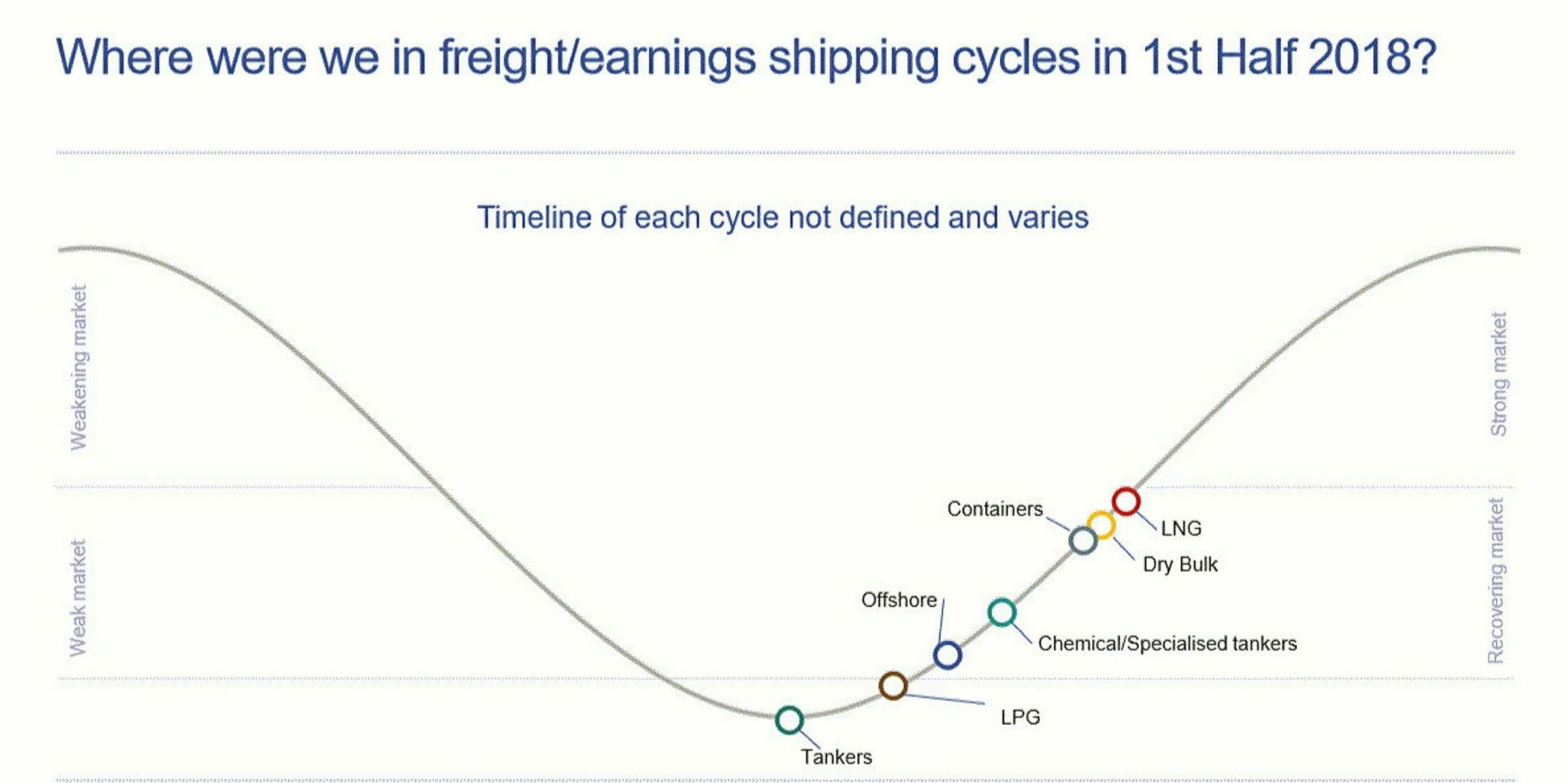

The world’s largest shipbroker places the LPG market ahead of only crude tankers on the recovery curve.

Its assessment of a shipping market recovery still has the sector behind offshore, chemical and specialised tankers, containers, dry bulk and LNG, which are all seen as further advanced after cyclical downturns.

Summer upturn puts gloss on figures

The VLGC market hit record highs in 2014 and 2015 but a flood of newbuildings ordered during the boom has since brought earnings down.

DNB Markets analysts, led by Nicolay Dyvik, note that VLGC rates are averaging $14,800 per day in the year to date.

Nicolay Dyvik: The third quarter is normally strong due to seasonal effects but, if high season sees VLGC earnings just in excess of cash break-even... there is a reason to be worried about rates into the fourth quarter and 2019

While this figure is glossed by an upturn in July and August, it is still down 7% year on year and below the bank’s forecast $20,000-per-day cash break-even of a VLGC newbuilding, Dyvik explained in a report this week.

“The third quarter is normally strong due to seasonal effects but, if high season sees VLGC earnings just in excess of cash break-even, we argue that there is a reason to be worried about rates into the fourth quarter and 2019,” he said.

DNB Markets’ forecasts suggest rates will fall from the $22,500-per-day average for July and August to $14,000 per day on average in the second half of this year. A minimal improvement to $15,000 per day is forecast for the first half of next year, before rising to $20,000 per day in the second six months.

DNB Markets is not alone in its caution. Experts tell TradeWinds that, despite the more positive conditions right now, there is still concern about the market rebalancing, given the newbuilding orderbook for 2019, when 22 VLGCs will be delivered, according to Clarksons.

“Some feel the extra LPG production coming out of the US will be enough [to lead a recovery]; others think otherwise,” one analyst said.

According to Dorian LPG, the orderbook stands at 13% of the trading fleet, with two more new ships set to be delivered this year.

However, a further 33 VLGCs, which will add around 2.7 million cbm of capacity, are slated for delivery by the end of 2020, the New York-listed shipowner added. It believes supply and demand fundamentals will rebalance during this period, although it was not specific as to when this might happen.

Rising fuel prices are complicating the picture for VLGC owners. Dorian LPG says the Baltic Exchange LPG Index in July exceeded $40 per tonne for the first time since February 2016.

However, Dorian LPG chief executive John Hadjipateras notes time charter equivalent rates sat at $35,000 per day in 2016 compared with $22,000 per day last month.

“The difference of course is due to higher bunker prices and this is a very vivid illustration of the vulnerability to higher bunker cost of non-eco ships,” he said on the company’s second-quarter conference call.