Shipping companies seeking to adopt vessel and voyage software performance benefits are being advised to do their homework as leading names warn of consolidation, mergers and even software companies going bust.

The industry’s digital disruption began in 2017, when start-ups, along with their private equity and venture capital investors, eyed potential in the fragmented and slow-to-adapt shipping, logistics and supply chain industries.

They saw similar opportunities to those offered by the financial markets a decade earlier and hoped to do what the likes of PayPal had for traditional financial transactions.

But wholesale disruption has not happened quite as hoped.

Software engineers thought they had discovered their PayPal moment when they identified the potential in garnering vessel data and selling advice to owners on ways to operate vessels and fleets more efficiently.

Dozens of solutions emerged but OrbitMI chief marketing officer David Levy said: “There is a lot of froth in this marketplace and a need to try to make some sense out of it.”

His company, a software spin-off from Sweden’s Stena Group, created a neutral platform to assimilate all the solutions in the market to help bewildered shipping executives make decisions.

It went as far as creating a service provider selection tool but did not get as far as listing what were hundreds of companies, some of which no longer exist or face consolidation.

The problem? Levy questions whether the usual private equity or venture capital playbook, which had disrupted finance, works in shipping, where investor expectations are of high returns in a short time.

As OrbitMI transitioned from its founding company, it secured investments from Galbraith, and more recently, Bureau Veritas has also acquired equity in the business.

“There’s not enough coming back for private equity,” Levy said. “What is needed is strategic investors as long-term partners.”

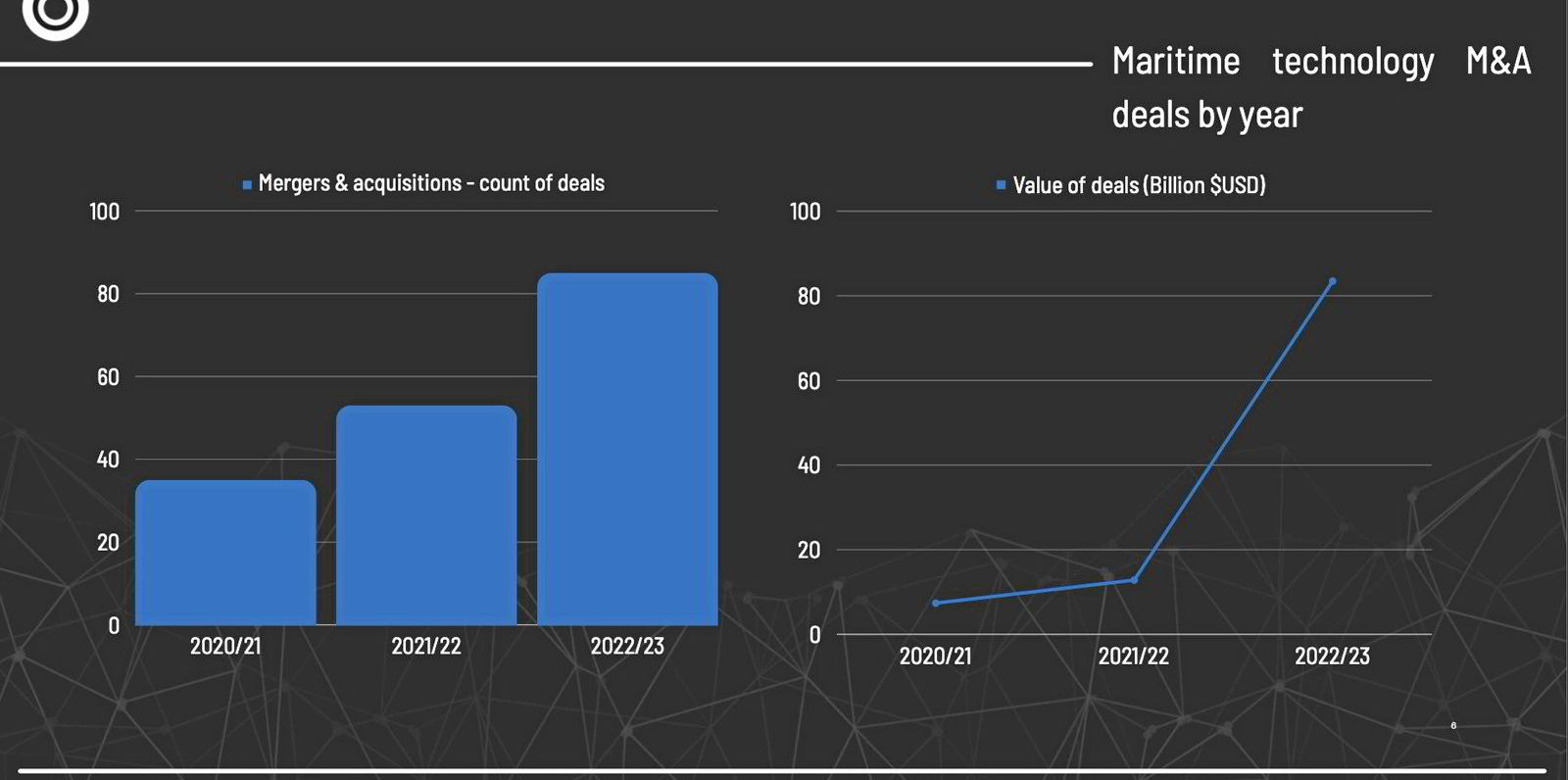

Last year, saw the fallout from this predicament with several high-profile digital acquisitions. Companies such as Veson Nautical, Danelec and ZeroNorth have been able to buy out other companies with available capital.

Not all digitalisation is equal

Giampiero Soncini, the developer behind AMOS — the first online maintenance system for shipping that was developed by Spectec in the 1990s — believes shipping has always had plenty of data.

But he said shipping has slowly warmed to using software as a service (SaaS) solutions, especially as it faces reporting and compliance requirements, fuel cost and transparency demands, and issues over crew workload.

Soncini moved on from SpecTec when it was sold to “buy and hold investor” private equity firm Volaris, which collects software firms including maritime players Shipnet, Helm and IDEA data solutions.

He is now managing director of Oceanly, another voyage data company, but openly wonders about the potential of the performance software market to make money.

It is simple mathematics, he told TradeWinds.

Many companies offer cloud-based SaaS solutions and the cost from a shipowner’s point of view would be a yearly fee of a few thousand dollars a year, per vessel.

“Given the limited number of commercial ships in the global fleet and the large number of software companies with solutions, the maths do not add up to large revenues for these software firms,” Soncini said.

Add to that the investment that has been made in the development of the software and one can see the imbalance. Huge investments and low returns.

“We are going to see much more consolidation,” said Casper Jensen, chief executive of Danish technology firm Danelec, shortly after the fire-sale acquisition of Nautilus Labs.

Positioning for an acquisition

Danelec is a hardware data company, known for its voyage data recorders (VDRs), which are now a mandatory part of a vessel’s equipment.

The VDR records a lot of information, including the vessel’s position, speed, direction and even engine movements, all collected from the onboard equipment.

For Danelec this is a goldmine of vessel information to be able to offer data to improve vessel performance, and the acquisition of Nautilus Labs as a software service was a natural fit.

Danelec was sold by its founder Otto Jakobsen in 2020 with Verdane Capital investing in the company. This gave Danelec capital to acquire Norwegian sensor maker Kyma and the VDR business of MacGregor in 2023. Then last year it pounced on the chance to secure Nautilus Labs.

Nautilus Labs was one of the darlings of the maritime software world, having had more than $50m invested in it by equity funds, notably one run by Microsoft, which pumped in most of this capital in a series of funding rounds over seven years.

The acquisition price has not been revealed, and Jensen said it will stay that way, but other digital experts have told TradeWinds the price is likely in the single-figure millions of dollars range, mostly because Nautilus Labs found it challenging to secure its own customer base.

But Nautilus Labs had been working with Danelec for over four years, said Jensen, and the potential to leverage Nautilus Labs’ expertise in AI and machine learning to enhance the company’s data collection capabilities presented a valuable addition to their offerings.

Jensen also suggested that Danelec and Verdane have the capital to be able to benefit from a consolidating market with further acquisitions.

Is investor appetite plummeting?

Investors took a shine to the supply chain and shipping start-ups in 2016, but according to start-up monitoring report Crunchbase, that interest has begun to dry up.

It calculated that investors around the world pumped over $50bn in seed investment or growth capital into software companies that offered performance analysis, or offered manufacturers’ insights into their logistics or supply chains, companies such as Flexport and Xeneta.

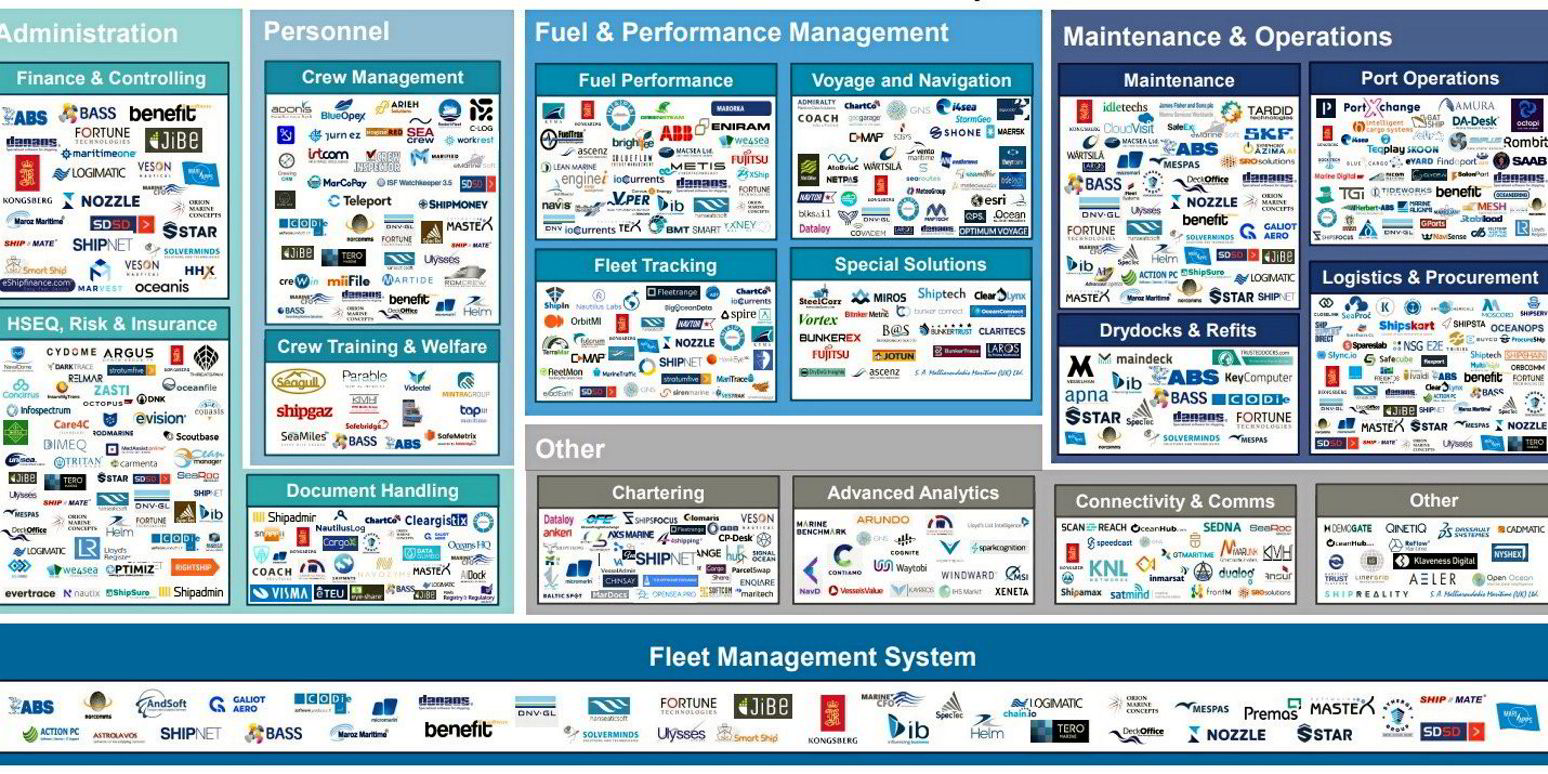

2023

- Seably (digital training) bought by Mintra Holding.

- UniSea acquires Maindeck.

- Danelec acquires Nautilus Labs.

- Danelec acquires MacGregors VDR (hardware data storage).

- ZeroNorth acquires/merges with Alpha Ori.

- Veson acquires VesselsValue.

- Marcura acquires ShipServ. (ShipServ was bought by Marlin Equity Partners, which had earlier invested in Marcura).

- Pole Star acquires StratumFive.

- Bureau Veritas acquires a stake in OrbitMI, a company spun out of Sweden’s Stena.

- Accel-KKR (owner of Navtor) acquires Voyager Worldwide.

- Navtor and Voyager Worldwide merge (both majority owned by Accel-KKR).

2022

- MacGregor acquires Kyma.

- Veson Nautical acquires Q88.

2021

- Alfa Laval buys StormGeo from EQT Partners. (EQT acquired a majority stake in StormGeo in 2014, buying off Reiten & Co, a Norwegian private equity firm, and TV2. DNV owning the remainder. StormGeo (while under EQT ownership) acquires Nautisk and AWT in 2014.

- Veson Nautical acquires Oceanbolt.

- Accel-KKR PE acquires Navis off Cargotec.

- Navis merges with Kaleris and Octopi, demonstrating supply chain and terminal interconnectivity.

2020

- Erma First acquires Metis Cybertechnology.

- Accel-KKRr buys into Navtor, merged Voyager Worldwide with Navtor in November 2023, Software company Ingenium Maritime in March 2022 (Digital log book) and Tres-Solutions in 2020.

Earlier

- 2017: Volaris acquires Shipnet.

- 2017: Lloyd’s Register acquires HanseaticSoft.

- 2016: Wartsila acquires Eniram (from Verdane PE, which is the current majority stakeholder in Danelec) for €43m.

- 2016: Volaris acquires SpecTec.

- 2014: ClassNK acquires Helm off ClassNK.

- 2014: ClassNK buys NAPA.

Last year, there were 208 funding rounds according to Crunchbase, compared with 446 in 2021, with total funding plummeting from $13bn to $2.1bn.

The result is layoffs from Flexport, the collapse of road freight start-up darling Convoy and construction supply chain start-up Katerra.

The same is also likely to begin happening in the shipping software space. Last year, there were at least a dozen mergers and acquisitions, and the expectation is there will be more to come.